M&A activity in the banking and payments area started to reheat in late 2020 following a collapse in the number of deals because of the Coronavirus pandemic. Notwithstanding, the domestic consolidation is driving this increase in deals, with cross-line investment deals still relatively small, partly because of their complexity and the numerous regulations included.

Without a doubt, figures from GlobalData reveal that cross-line activity accounted for just 26% of the deals that occurred over the second from last quarter of 2020. The data shows that there were 153 deals, worth $10bn, in the second from last quarter, up from 141 ($7.4bn) in the subsequent quarter and 165 ($8.9bn) in the first.

The potential impact of the EU's banking association

FICO score agency Extension states that possibilities for cross-line M&A in general are improving, although it "keeps on being skeptical in terms of the cross-line bank mergers, yet sees the chance at least on paper of more attractive financial rationales".

Progress on banking association in Europe, which would see barriers to cross-line M&A lifted, could mean the banking landscape will look totally different in a couple of years from what we see today. EY

Nonetheless, Degree adds that "the completion of the banking association [within the EU], including a working store guarantee scheme that would uphold the rationale of such deals and encourage more cross-line risk sharing, seems to move glacially".

To be sure, EY seems to share the same view about the positive impact of the banking association on cross-line deals. It says: "Progress on banking association in Europe, which would see barriers to cross-line M&A lifted, could mean the banking landscape will look altogether different in a couple of years from what we see today."

In any case, the head of Germany's Federal Financial Administrative Authority, Felix Hufeld, told business newspaper Handelsblatt that the completion of a banking association in Europe along with the establishment of a joint store security scheme isn't a precondition for cross-line bank mergers. By and by, he added that elevated degrees of complexity is a vital reason behind the ongoing low number of M&A deals.

Eyes on domestic bank consolidation

Regardless of the increase in cross-line M&A on a global level in both value and volume during the second from last quarter of 2020, it actually compares ineffectively when compared with domestic M&A, and this activity has driven the recuperation in the banking and payments M&A market.

Figures from GlobalData show that there were 588 deals in banking and payments at a global level during the second from last quarter of 2020, up from 540 in the subsequent quarter, however down from 651 deals in quarter one. In terms of the deal value, it amounted to $61.6bn in the second from last quarter, up from $47.6bn in quarter two.

The Investment Monitor analysis shows that 74% of the deals that occurred in the second from last quarter were domestic, amounting to 83.8% of the deal value that was contributed over the three months. This demonstrates that domestic M&A activity and consolidation has become something of a pattern amid the pandemic for financial backers hoping to lessen costs and generate economies of scale.

"We figure the drive to consolidate domestically is steady for credit," said Marco Troiano, analyst for Italian and Spanish banks at Degree, in a public statement. "It improves the banks' market positions and estimating power and allows a faster decrease of expenses. It also allows greater economies of scale in IT investment and innovation."

What's more, GlobalData reports that inside banking and payments M&A activity, "domestic consolidation remains an agenda for regulators for diminishing expenses, with the CaixaBank-Bankia merger in Spain being a notable example of that. Diminished operational uses will also help in weathering the Coronavirus impact. Meanwhile, this challenging period offers open doors for cash-rich purchasers to profit from troubled valuation". Different examples of domestic takeovers incorporate Intesa Sanpaolo acquiring UBI Banca in Italy in the early months of 2020.

Southern European banks' ascent on the radar

Rating agency Extension states that the ongoing spotlight on banking M&A activity in Europe falls on Spain and Italy, which are "nations with fragmented banking markets and large branch organizations, where the money saving advantages and the strategic feeling of consummating domestic tie-ups have sparked a free for all of activity and speculation about how the extremely past due course of consolidation will play out".

What's more, EY observes that another factor behind this consolidation is a worry over profitability, particularly among the weaker banks in Europe. "This has been exacerbated by the ascent of non-performing loans because of Coronavirus and an acknowledgment that investments in digitisation and a more fundamental transformation need somehow to be supported and accelerated," says the EY site.

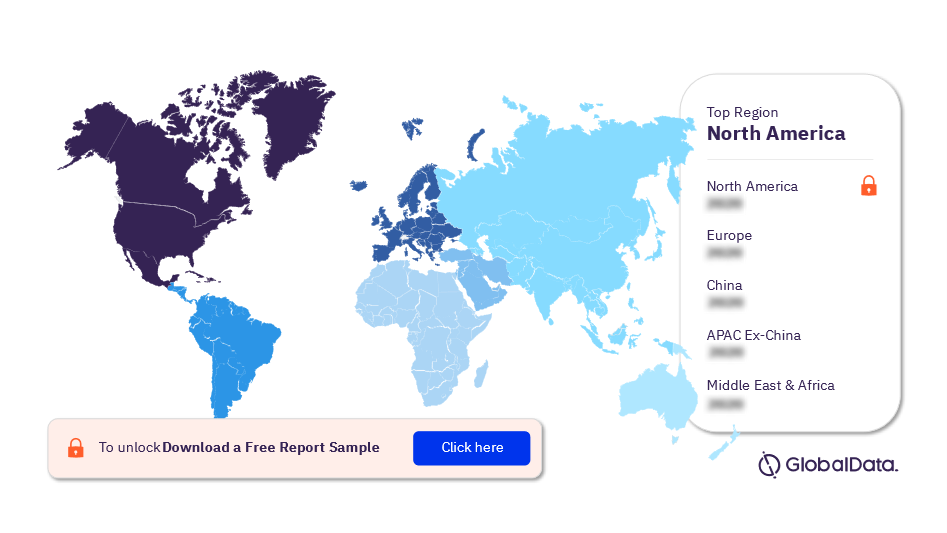

Figures from GlobalData feature that Europe was second in terms of deal activity in the banking and payments area in the second from last quarter of 2020, recording 158 deals with a value of $13.9bn, with North America encountering the most elevated M&A activity in the area. For sure, North America recorded 253 deals worth $33.7bn in this period, with Asia-Pacific in third with 137 deals worth $12.5bn. There were 27 deals in the Middle East and Africa, and 16 deals in South and Central America.

With financial administrations financial backers hoping to waterproof their investments amid the Coronavirus pandemic, apparently Banking And Payment Industry M&A Deals activity is being utilized to reduce expenses, transform troubled assets and increase operational productivity. In any case, delays to any banking association in Europe as well as the complexity of cross-line deals explain the dominance of domestic deals as the appetite for consolidation gets larger.